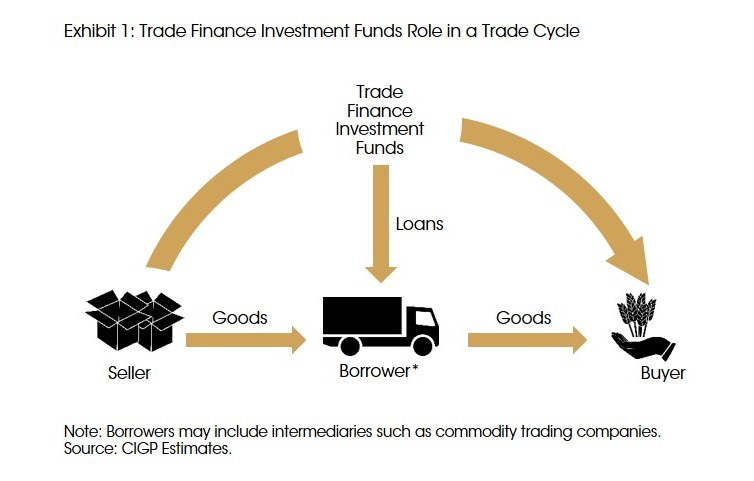

Focus: Introducing Trade Finance as an Asset Class

Rensi Widjaja

The function of trade financing is an essential tool to the workings of the global economy; it is a key enabler in international trade and globalization. Around 80% of global trade transactions require a form of financing. Insufficient financing and working capital pressures could bring about missed growth opportunities for businesses that could eventually stagnate an economy. This is particularly true for small and medium sized enterprises (SMEs) who face the greatest challenges in accessing the benefits of trade financing. The World Trade Organization (WTO) notes that SMEs account for ~20% of US exports, and ~40% of EU exports. Around 60% of trade finance requests from small businesses are rejected by banks.

In its annual global survey report published in 2018, the International Chamber of Commerce (ICC) highlighted regulatory issues as one of the top concerns among its respondents comprising of 251 banks in 91 countries. The introduction of Basel II and III has seen major global banks shy away from their trade financing businesses. The Basel Accords, which were developed as a response to 2008 financial crisis, have heightened banking regulation especially as it relates to capital requirements. On top of regulatory pressure, banks are also facing competition over pricing in traditional trade financing contracts which has prompted them to abandon deals that may be unprofitable and the banks have subsequently reigned in exposure to this space.

These issues have accumulated into a gap between supply and demand in trade finance which provide an opportunity for money managers to create an investment vehicle and instruments to service trade finance customers. According to the WTO, globally, the difference is estimated to be as high as USD 1.5 trillion per annum as of 2018. These underbanked shippers, suppliers, buyers and intermediaries have led to the emergence of some quality trade finance investment funds. Still a relatively new concept in the industry, there are only around 15-20 trade finance funds globally with aggregate AUM of less than USD 10bn according to RedBridge.

China and the Trade-Finance Pivot

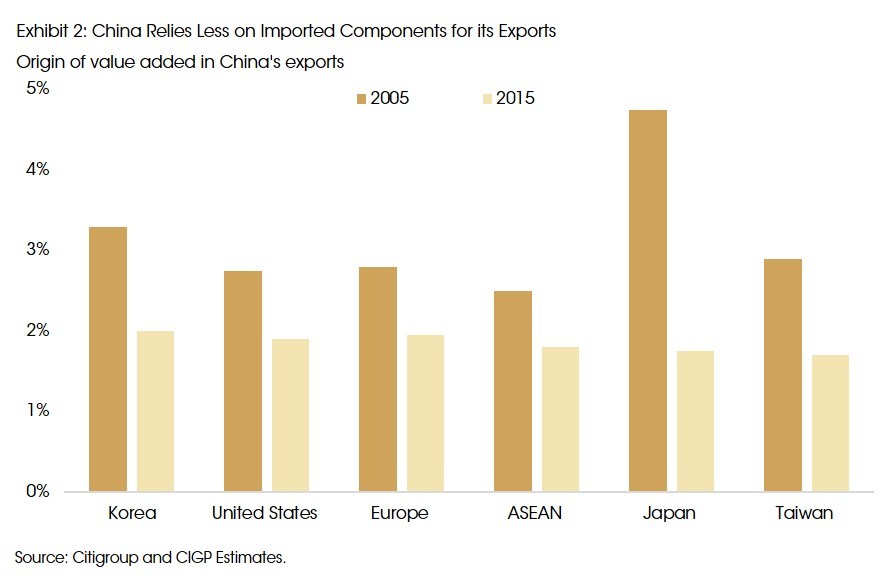

As a result of the ongoing trade feud between the US and China, the word “trade” is not always greeted with enthusiasm by investors. We think that the US-China trade war should have minimal impact on trade finance and therefore trade finance investment vehicles. In fact, not many trade finance funds have exposure to specific US-China trade finance deals. Moreover, we observed that fund managers are pivoting away from China related deals to find alternatives in other major trade hubs such as South East Asian countries that are seeing a boost in activity due to multi-national companies shifting their manufacturing. Furthermore, an August report from LGT highlights that China has reduced its reliance on imported components for its exports. This could also explain why there are less trade finance needs from China than investors might have expected. See Exhibit 2.

Contract Risks

Amongst other traditional commercial banking products, trade finance is generally considered to be less risky. The space recorded default rates as low as 1% in 2018 according to the ICC. One distinct observation from our research is that most trade finance funds do not facilitate finished goods, but rather facilitate trade and transport in raw materials, many of which are commodity-like products and are freely traded on liquid secondary markets. This acts as a backstop to failed contracts where one party may not follow through, thereby creating a domino effect. Frequently funds will act as intermediary to connect buyer and seller in the event of a failed trade thereby attempting to recoup losses. Hence the recovery rates in trade financing are ordinarily greater than they are in traditional consumer lending. In sum, these factors generally result in stable returns of trade finance funds of approximately 5 – 7% per annum.

Risk Reduction Mechanism: Block Chain

We found that trade financing businesses are still relatively clustered around antiquated processes, such as: lengthy forms, sending copies between parties, requiring multiple sign-offs, and checking insurance terms. Consequently, our sources acknowledge that digitalization plays an important part in transforming the trade finance industry to be more efficient with respect to costs, security and time. However, the uptake is limited due to scale and mass appeal. Change is challenging. Block chain works best when every party is participating. After all block chains build over time due to buy-in and contributions of data from all involved parties. In terms of our preferred ways to take advantage of this trend we favor managers who have a superior infrastructure set up that includes fully automated end-to-end process from client on boarding to the monitoring of shipment of goods. This back-end support is a crucial as one part of many in the broader ecosystem within the fund. Adoption of block chain technologies in trade finance will likely make this space more attractive over time.

Investment Options

According to data from a trade finance fund-of-fund, the trade finance fund category recorded a low correlation to both equities and bonds. The correlation, over a period of 6 years from 2013-2019, with the MSCI World Index is approximately 0.23, and is approximately 0.15 with the iBoxx Investment Grade Bond Index. In 2018, we found that trade finance funds returned on average 5-7% p.a. while the MSCI World Index returned -10% and iBoxx Investment Grade Bond Index returned -7%. This suggests that trade finance has a low correlation to stocks and bonds and therefore can be a good diversification tool.

In the midst of an increasingly volatile market, we continue to favor solutions with low correlation of returns to traditional asset classes. The abandonment of global banks of trade finance services has created opportunity for investors. Trade finance is a unique investment type and should be considered as an important part of a diversified portfolio allocation. We believe trade finance funds offer an attractive opportunity. In particular, we favor a trade finance fund offering a distinct solution in Asia.

Sources: Bank for International Settlements (BIS), Citigroup, International Chamber of Commerce (ICC), LGT Private Bank, Redbridge, World Trade Organization (WTO) and CIGP Estimates.